| NO | TYPE OF LICENSES | DOCUMENT LINKS |

|---|---|---|

| 1 |

List of Business fields that have to do presentation to BKPM before applying the Principle License |

Download |

| 2 |

Application form and required document: |

Download |

| 3 |

Application form and required document:

b. Amendment of principle license

|

Download |

| 4 | Application form and required document: c.Merger principle license |

Download |

| 5 |

Application form for Business License

|

Download |

| 6 |

Application form for Importer Identification Number (API)

|

Download |

| 7 | Required document for Business Licenses: a. Business Licenseb. Amendment of Business License (Change on project location) c. Amendment of Business License (Change on business fields) d. Amendment of Business License (Change on license duration) e. Merger business license f. Employment Training Institution (LPK) Business License g. Extension of Employment Training Institution (LPK) Business License h. Amendment of Employment Training Institution (LPK) Business License i. Business License of Domestic Worker Placement Service in Indonesia j. Extension of Business License of Domestic Worker Placement Service in Indonesia k. Amendment of Business License of Domestic Worker Placement Service in Indonesia l. Worker Provider Service Business License m. Extension of Worker Provider Service Business License |

Download |

| 8 | Required document for Representative Offices: a. General Foreign Representative Office (KPPA) b. Amendment of General Foreign Representative Office (KPPA) c. Tentative Foreign Trade Representative Office Business License (SIUP3A) d. Permanent Foreign Trade Representative Office Business License (SIUP3A) e. Extension of Foreign Trade Representative Office Business License (SIUP3A) f. Amendment of Foreign Trade Representative Office Business License (SIUP3A) g. Foreign Construction Service Company (BUJKA) h. Extension of Foreign Construction Service Company (BUJKA) i. Closing of Foreign Construction Service Company (BUJKA) j. Amendment of Foreign Construction Service Company (BUJKA) k. Producer Importer Identification Number (API-P) l. General Importer Identification Number (API-U) m. Office branch |

Download |

| 9 | Application form and required document for investment facilities: a.

Import Duty Facility on Machinery |

Download |

| NO | TYPE OF LICENSES | DOCUMENT LINKS |

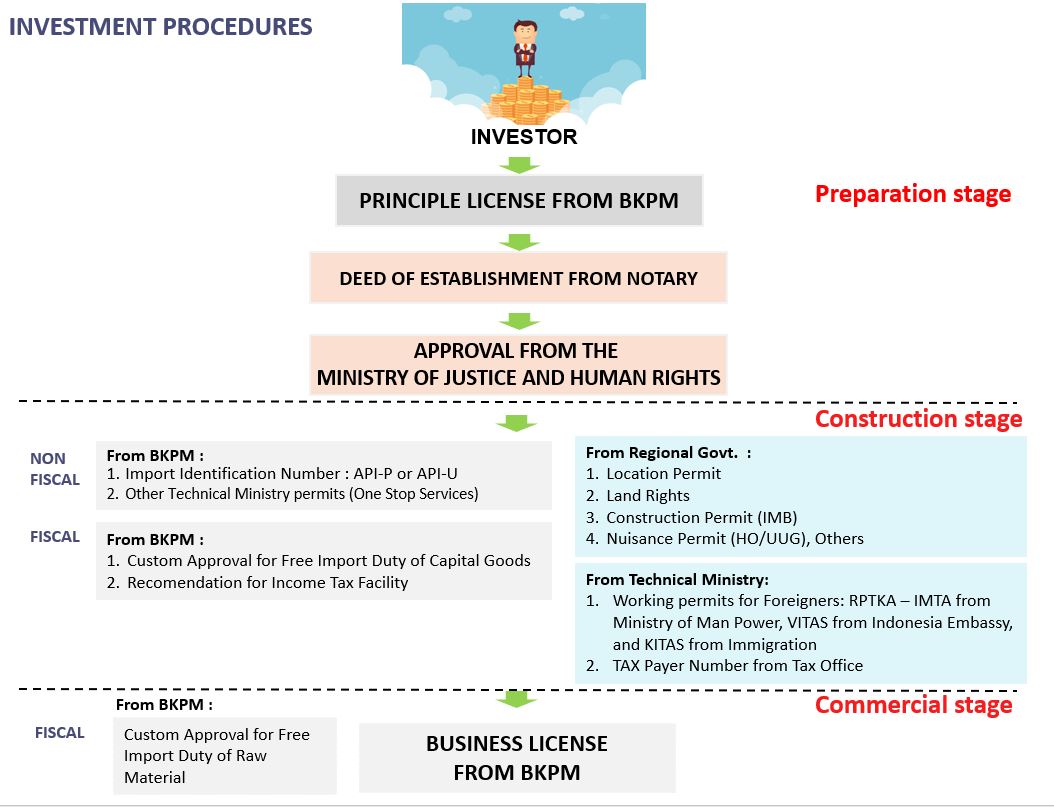

How do I establish a company in Indonesia?

1. PRINCIPLE LICENSE

₋ First, you have to issue Principle License (Izin Prinsip or IP) at BKPM One-Stop Service-Center or OSS-C (Pusat Pelayanan Terpadu Satu Pintu or PTSP Pusat).

₋ When you want to invest in Indonesia, first you have to check whether your business is open for FDI in Indonesia in accordance to the Indonesia Investment Guidance (Daftar Negatif Investasi or DNI) under the Presidential Decree No. 44 of 2016 that stipulates the sectors which are closed and open with conditions to investment. If the business sector is not listed in the DNI, the business will be considered open and allowed for up to 100% foreign ownership. If the business sector is open or open with a condition, the foreign investor will be able to apply for Principle License (IP), to begin the investment process, subject to the condition stated in Indonesia Investment Guidance (DNI).

₋ All applications for Principle License (IP) will be done through the BKPM-Online Service Platform or Electronic Investment Information & License Service (SPIPISE) [http://online-spipise.bkpm.go.id]. All investors will always be able to approach the BKPM office for advice and assistance in the application process.

₋ Once the Principle License (IP) is approved by BKPM OSS-C, the investor will be able to set up its business entity by engaging any public notary office to draft the establishment of an FDI Company (PT.PMA), which is called Company Deed of Establishment. This draft will need to be ratified by the Ministry of Justice and Human Rights of the Republic of Indonesia to be legalized and officially posted in the state gazette.

2. DEED OF ESTABLISHMENT

₋ After that, you can establish the legal entity of your company in Indonesia by engaging a public notary to issue a Deed of Establishment. The Deed of Establishment of FDI Company (PT. PMA) could be issued by a public notary in Indonesia and it is prepared in Bahasa Indonesia.

₋ The Deed of Establishment contains the following information:

1. Name and address of the company.

2. Line of business of the company.

3. The articles of association.

4. The composition of the Board of Directors or BOD (Dewan Direksi) and the Board of Commissioners or BOC (Dewan Komisaris) of the company.

5. The identity of the company shareholders and the share of ownership.

₋ The legal entity of the FDI Company should be a Limited Liability Company or Ltd. (Perseroan Terbatas or PT). The ‘PT’ company should be owned by a minimum of 2 parties; each party is either individual or corporate. According to Indonesian law, any company with any percentage of foreign shareholding is considered as an FDI Company or foreign-owned-PT-company, in short, ‘PT. PMA’.

₋ After the establishment of the legal entity, the public notary will register the new PT. PMA to the Ministry of Justice and Human Rights of the Republic of Indonesia. Once registered, the establishment of the new PT. PMA will be published in the state gazette.

₋ The ratification of legal entity by the Ministry of Justice and Human Rights of the Republic of Indonesia will serve as the basis of the establishment of PT. PMA. From this point, the PT. PMA will be able to start setting-up the company infrastructure and related operational licenses.

Note:

1. Before establishing the PT. PMA, you should check the availability of the company name that you want to set up from the Ministry of Law and Human Rights of the Republic of Indonesia through a public notary in Indonesia.

2. Concerning applications of any licenses from BKPM or other government institutions in Indonesia, all information on the application has to refer to the Deed of Establishment of PT. PMA. Any changes in company condition which are not relevant to the Deed of Establishments, such as change or expansion of the business sector, change of company location or business activity location, should be informed to the BKPM and related government agencies to get licenses amendments.

3. OTHER LICENSES (TECHNICAL MINISTRY AND REGIONAL LICENSES)

₋ After establishing the FDI Company Deed, the investor will also be able to apply for the necessary Technical Ministry and Provincial Government Licenses (regional regulation), such as:

1. Taxpayer Identification Number or Tax ID (Nomor Pokok Wajib Pajak or NPWP), can be applied through the online service of Indonesia Directorate General of Taxes at https://ereg.pajak.go.id (currently the service is only available in Bahasa Indonesia).

2. Regional licenses, such as Company Domicile Certificate (Surat Keterangan Domisili Perusahaan or SKDP), Environmental License, Building Permit (Izin Mendirikan Bangunan or IMB), Nuisance Ordinance Permit, and Location Permit can be obtained from the local or regional authority where the PT. PMA is located and applicable through the office of building management or industrial estate management.

3. General Importer Identification Number (Angka Pengenal Importir Umum or API-U) or Producer Importer Identification Number (Angka Pengenal Importir Produsen or API-P) is applicable through BKPM OSS-C.

4. Foreign Worker Employment Permit (IMTA) applies online to the Ministry of Manpower through link http://tka-online.naker.go.id.

5. Other technical licenses, an investor with the legal business entity will be able to process all the required licenses from technical ministries through One-Stop Service center at BKPM. High officials from 22 technical ministries and government agencies will be positioned in BKPM to attend to all investment inquiries and also application of the technical licenses about their business sector.

4. BUSINESS LICENSES

₋ Once the company is ready for Commercial Stage, the FDI Company will be able to apply for its Business License (IU) from BKPM OSS-C to start its business operation.

Additional Notes:

1. All foreign investors who set up business entities are mandatory to submit the Investment Activity Report (Laporan Kegiatan Penanaman Modal or LKPM) periodically to BKPM.

2. The FDI Company will need to update the LKPM every quarterly during its setting-up period (after owning Principle License or IP) and biannually after receiving its operational (after owning Business License or IU).

The group includes coal mining; mining on the ground or underground and through the method of liquefaction and cleaning, gluing, dozing, compaction, etc. to classify and improve quality or to facilitate transportation. This activity also includes the search for coal from the culm bank.

This subgroup includes:

a. Coal mining, such as mining on the ground or underground

b. including liquefaction mining

c. Cleaning, gluing, crushing, and compacting coal

d. Classification, improve quality or ease shipping and storage

e. Search for coal from a collection of bank culm

This subgroup does not include:

a. Lignite mining

b. Soil (peat) excavation and agglomeration

c. Coal experiment drilling

d. Coal mining support services

e. Charcoal stove to produce solid fuel

f. Coal briquette fuel processing industry

g. Work to develop or prepare the property for coal mining.

The group includes mining operations, drilling of various quality coal such as

anthracite, bituminous and sub-bituminous both mining on the ground or

underground, including liquefaction mining. These mining operations include

excavation, crushing, washing, filtration, and mixing also

compaction which is improves quality shipping

and

storage.

Including the search for coal from a collection of bank culm.

This basic group includes crude oil production, mining, and extraction of oil from oil shale, oil sands, natural gas production, and the search for hydrocarbon liquids. This basic group also includes operations and/or development of oil and gas mining locations.

PETROLEUM MINING

This group manages crude oil and operations or development petroleum locations such as drilling, planning and installing equipment on the oil wells, and oil preparations from production sites to shipment. This group does not include petroleum refining activities.

PETROLEUM MINING

This subgroup includes:

a. Crude petroleum mining

b. Bituminous mining or oil flakes and asphalt sand

c. Production of crude oil from bituminous flakes and sand

d. Production of condensate oil (petroleum with high carbon content)

e. Processing to produce crude oil, such as collecting, filtering,

dry, stabilization, and others.

This subgroup does not cover:

a. Oil and gas mining support services

b. Oil and gas exploration services

c. Petroleum processing industry

d. LPG production from petroleum refineries

e. Operation of the pipeline

PETROLEUM MINING

This group includes crude petroleum mining operations or activities including petroleum extraction business, drilling, mining, separation and shelter, condensate crude oil production, processing to produce crude oil by storing, filtering, drying, stabilizing and others. The results of petroleum mining include crude oil and condensate. This group also includes bituminous sand mining operations (oil shale) and asphalt sand. These mining activities include excavation, drilling, crushing, washing, filtering and mixing and storage. Including the production of crude petroleum from oil shale and bituminous sand if related to mining.

NATURAL GAS MINING AND GEOTHERMAL ENGINEERING

This group includes the production of gas and liquid hydrocarbons through the liquefaction method and coal pyrolysis at the mining site. This group also includes gas condensate extraction, separation, and flow of liquid hydrocarbon fractions and gas desulfurization, and geothermal search and drilling activities.

NATURAL GAS MINING AND GEOTHERMAL ENGINEERING

This subgroup includes:

a. Production of crude hydrocarbon gas (natural gas)

b. Mining of condensate gas (gas dew)

c. Drying and separating parts (fractions) of liquid hydrocarbons

d. Gas desulfurization

e. Liquid hydrocarbon mining produced through liquefaction or pyrolysis

f. Geothermal search and drilling activities

This subgroup does not cover:

a. Oil and gas mining support services

b. Oil and gas exploration services

c. LPG production from refining petroleum

d. Industrial gas industry

e. Operation of the pipeline

NATURAL GAS MINING

This group includes natural gas extraction, drilling, mining, separation, and shelter. The results of mining natural gas include natural gas. Liquefaction of natural gas into LNG until shipping is still included in activities mining. Including the activity of Coalbed Methane.

GEOTHERMAL ENERGY ENTERPRISES

This group includes geothermal search and drilling activities. Including other activities related to the operation of geothermal power to its utilization place.

All investment projects of Foreign Direct Investment or FDI as well as Domestic Direct Investment or DDI (Penanaman Modal Dalam Negeri or PMDN) projects which are approved by BKPM or by the office of investment in the respective districts, including existing FDI and DDI companies expanding their projects to produce similar product(s) in excess of 30% of installed capacities or diversifying their products, will be granted the exemption from Import Tax so that the final tariffs will become 0%. This facility applicable on:

1. The importation of capital goods including machinery, equipment, and auxiliary equipment for an import period of 2 years, started from the date of the decision determined.

2. The importation of goods and materials or raw materials regardless of their types and composition, which are used as materials or components to produce finished goods or to produce services for the purpose of 2 years full production (accumulated production time).

3. The importation of machines, goods, and materials which:

- Are not produced in Indonesia.

- Are produced in Indonesia but they don’t meet the required specifications.

- Are produced in Indonesia but the quantity is not sufficient for the need of the industry.

The exemption of import tax will also be granted to the importation of capital goods of electricity for an import period of 2 years and can be extended by a maximum of 1 year. This facility is not applicable for transmission, distribution, support services, and repairing equipment.

For the importation of goods in term of Contract of Work or CoW (Kontrak Karya or KK) or Coal Mining Business Work Agreement (Perjanjian Karya Pengusahaan Pertambangan Batubara or PKP2B) will be granted the exemption and/or relief from import duty based on the contract.

The application can be requested by attaching a recommendation letter from Directorate General of Mineral and Coal, Ministry of Energy and Mineral Resources of the Republic of Indonesia.

Based on the latest Government Regulation No. 18 of 2015, about Income Tax facilities for investment in certain business sectors and/or in certain locations, the domestic and foreign investors will be granted tax allowances in a certain sector and/or area. This latest regulation replaces its previous preceding Government Regulation No. 52 of 2011.

Facilities provided by the new Government Regulation No. 18 of 2015 are:

1. Reduction of net income by 30% of the total investment in the form of tangible fixed assets, including any land that is used for the business main activities, shall be charged for 6 years, respectively at 5% per year calculated from the commencement of commercial production.

2. Accelerated depreciation on tangible assets and amortization of intangible assets acquired in the framework of new investment and/or business expansion, with the useful lives and depreciation rates as well as amortization rates.

3. The income tax on dividends paid to any non-resident taxpayer other than the form of a permanent establishment in Indonesia in amount of 10% or lower tariffs in accordance with any applicable double taxation treaty.

- A company located in the Industrial Area and/or

Bonded Zone.

- A company operating in construction development for

infrastructure sector.

- A company that use domestic raw materials at least

70%.

- A company that is absorbing 500-1,000 of domestic workforces.

- A company that is conducting research and development (R&D).

- A company that is doing a re-investment.

- A company that exports at least 30% of its sales value.

For detailed information on the list of business sectors that are eligible for tax allowance, please refer to Attachment I & II of Government Regulation No. 18 of 2015. There are 66 business sectors listed in Attachment I and 77 business sectors listed in Attachment II.

PROCEDURE ON THE APPLICATION FOR TAX ALLOWANCE (New Applicant)

For new applicant or application of new project for tax allowance, listed below is the framework on the application procedures:

Note:

The following procedures are the simplified framework of the tax allowance

application procedure. The full and complete details of it are available in the

Regulations of Chairman of BKPM No. 18 of 2015.

EXPORT MANUFACTURING:

There are many incentives provided for exporting manufactured products. Some of these incentives are:

BONDED ZONES

The industrial companies which are located in the bonded areas are provided with many incentives as follows:

FREE TRADE ZONES

The companies operating in Free Trade Zone or FTZ (Zona Bebas Perdagangan) areas enjoy several incentives such as exemption of import duty and excise, import-related taxes (VAT, Withholding Tax/ Income Tax) not collected. Additionally, FTZ also offerS faster issuance on investment-related licenses and immigration clearance in terms of foreign employees. The limitation for operating in FTZ is that exporting goods out of FTZ into the Indonesian customs area will apply the tax duty and excise back on the previously duty exempted goods.

TAX HOLIDAY FACILITIES

According to the Regulation of the Ministry of Finance No. 159/PMK.010/2015 and the Regulation of the Chairman of BKPM No. 19 of 2015 the applicant or company should meet the following criteria:

It is, then, eligible for the following incentives:

| Test |